Share Code: ARA – Market Cap: R498m – Discount to NAV: 42%

FY 23 Results: A Mixed Bag of Results

- Astoria’s USD Net Asset Value (NAV) felt pressure and slipped marginally to $0.7947 per share (FY 22: $0.8266 per share), though the Rand NAV was slightly up at 1454cps (FY 22: 1406cps) as the Rand weakened over the period.

- A decline in diamond prices was a headwind on diamond interests, loadshedding hurt Goldrush’s LPM performance & Leatt’s share price followed its sales down over an extra-ordinary trading period.

- On the other hand, Outdoor Investment Holdings (OIH) traded (really) strongly (see relative sales performance below), ISA Carstens saw +10% enrolment growth & Vehicle Care Group (VCG) is proving its model nicely.

Commentary: Conservative NAV & Upside Optionality

- Other than valuing A-Tec in OIH separately as a Norwegian asset and lifting ISA Carsten’s Academy multiple from 6.0x to 7.0x (but it remains well below other listed educational stock multiples), Astoria’s unlisted valuations remain largely consistent with history and, arguably, conservative.

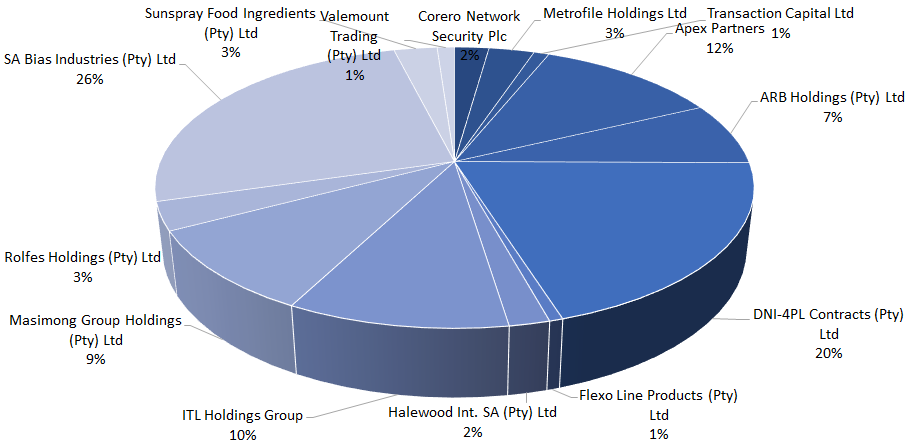

- A FY 24E normalisation in diamond prices & in Leatt Corp’s trading environment could point to upside in Astoria’s NAV (Leatt & diamond interests are a third of the Group’s NAV).

Valuation, 12m TP & Implied Return: Above Average Discount

- Updating Astoria’s NAV to current prices, the share is trading at an above-sector-average c.42% discount to current NAV (Previously: 34%) despite its strong growth in NAV (+32.4% y/y CAGR in Rand-NAV since management took over on 1 December 2020)

- If we take out our calculated “HoldCo discount” of c.13.9% (Previously: 15.0%) from this NAV, we arrive at a fair value for Astoria’s shares of c,1192cps (Previously: 1152cps) or c.49% higher than the current share price.

- Rolling this fair value forward at our Cost of Equity, we arrive at a 12m TP of c.1420cps (Previously: 1365cps) which implies a potential return of c.77% from the current share price.