Share Code: SBP – Market Cap: R3.5bn – Dividend Yield: 1.1%

FY 24 Results: Excellent Results

- Sabvest’s Net Asset Value (NAV) increased to R5bn, up 18% from R4,3bn and, amplified by share buy-backs at below-NAV prices, the Group’s Net Asset Value per share (NAV ps) increased by 21% to 13213cps (FY 23: 10936cps).

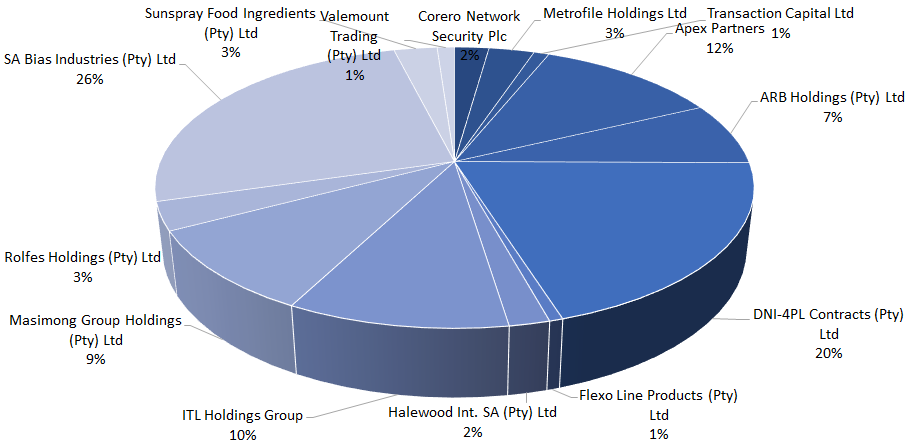

- Major contributors to the NAV increase include strong performance from almost all investees, particularly ITL, which experienced a material fair value gain as the labelling group (finally) recovered strongly following the draw-out apparel sector post-COVID recovery.

- Major realizations during the period include Metrofile, Rolfes, WeBuyCars, and (a partial exit of) Sunspray.

- Share buybacks amounted to R59.9m (2023: R11.8 million) for 850 000 SBP shares (VWAP was c.7047cps).

Thoughts: Positive Momentum Going Forward

- Growing investee profitability, central degearing annualizing and, possibly, further opportunistic share buy-backs are all promising for per share NAV growth in the coming period.

- Furthermore, we expect good NAV growth to be particularly driven by positive performances in Apex Partners (DRA Global’s unlock) and the ITL Holdings Group (recovery shifting to growth).

- It is worth note that the consistent execution of profitable exits at or above book value further supports our view of the sturdiness of the Group’s NAV.

Valuation, 12m TP & Implied Return: Discounted

- We estimate that the share is currently trading at a c.31% discount to its current 13108cps NAV and—after including a HoldCo c.10% discount against this NAV of 10% (unchanged)—we believe that the share’s fair value is around 11798cps (previously: 10754cps).

- Rolling our post-discount fair value forward, we see the Group’s 12m TP as 14017cps (previously: 12616cps) with an implied return of +55% from these levels.